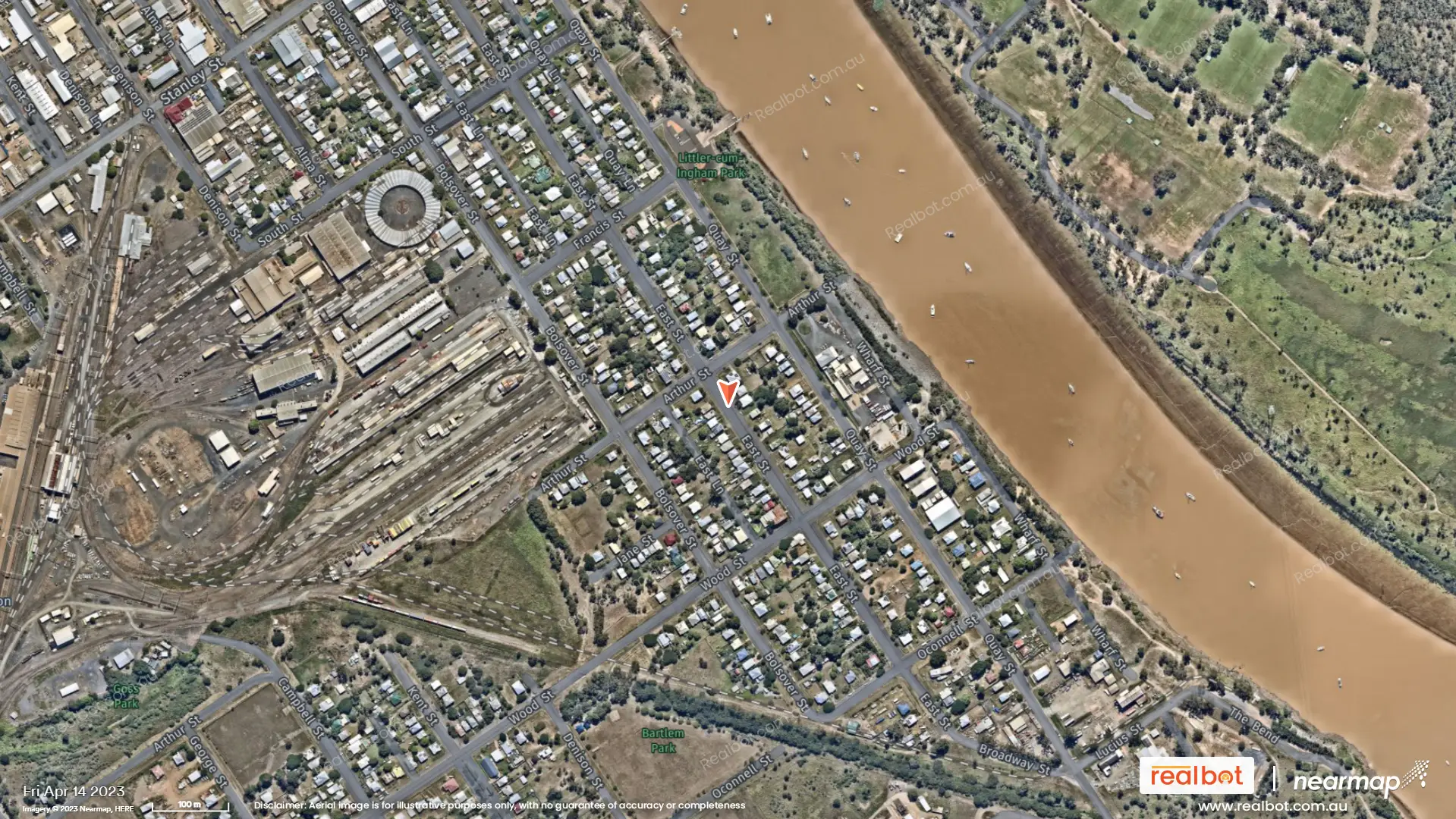

One of Rockhampton's earliest residential settlements, Depot Hill was developed to house workers for the nearby railway and river wharves. The suburb is characterized by traditional 'high-set' Queenslander architecture, a direct response to the region's tropical climate and flood history.

Today, it remains a low-socioeconomic residential area with a gritty, industrial-fringe character, popular with budget-conscious investors and long-term locals.

- Exceptionally low entry-level purchase prices.

- High gross rental yields often exceeding 8%.

- Walking distance or short drive to Rockhampton CBD and riverfront.

- Character-filled heritage housing stock with renovation potential.

- Strong community spirit among long-term residents.

- Prohibitive or unavailable flood insurance premiums.

- High risk of total property inundation during Fitzroy River peaks.

- Significant maintenance costs associated with older timber homes in flood zones.

- Stagnant long-term capital growth due to risk-averse buyer pool.

- Higher than average local crime statistics and social vulnerability.

How this suburb feels day-to-day.

Dominant dwelling stock.

Typical entry to ceiling.

Depot Hill offers a unique 'high-risk, high-reward' scenario. While the entry price is among the lowest in the country for a city-fringe location, the recurring cost of flood recovery and insurance makes it a complex asset for inexperienced buyers.

$220,000 – $330,000

N/A (Limited stock)

12-month movement

Current asking rents

Prices are heavily suppressed by the 'flood discount.' While the rest of Rockhampton has seen stronger growth, Depot Hill remains a niche market for cash-buyers and yield-seekers.

Price comparison

Median price ÷ median income

Estimated rental yield

While the purchase price is low, the 'true' affordability is lower when factoring in insurance premiums that can exceed $10,000 per annum, if available at all.

Lower = tighter market

Avg time on market

Annual rental increase

Low-income workers, families seeking budget housing, and social housing tenants.

Strong cash flow is the primary driver. Investors must account for higher-than-average depreciation and repair costs due to the environment.

- General spillover from Rockhampton's broader economic growth.

- Extreme shortage of low-cost rental accommodation.

- Potential for long-term flood mitigation infrastructure (though controversial).

- Gentrification of the nearby Rockhampton CBD riverfront.

- Increasingly difficult lending criteria for flood-prone postcodes.

- Rising cost of building materials for heritage repairs.

- Climate change projections increasing flood frequency.

Growth is expected to underperform the Rockhampton average as insurance costs become a primary barrier to resale. It will remain a high-yield, low-growth 'cash cow' market.

vs last 12 months

Relative comparison

Prioritize properties with secure fencing and security screens. Local knowledge of specific streets is vital as safety can vary block-by-block.

The suburb is defined by its relationship with the Fitzroy River. Environmental risk is the primary factor in all property decisions here.

Severe. The suburb is a natural flood basin. Major events (e.g., 2011, 2017) see widespread property inundation.

Low risk; primarily an urban/industrial interface.

Critical issue. Many standard insurers will exclude flood cover or charge premiums that make the investment unviable.

Flood Hazard Overlay (Extreme), Heritage Overlay (Select Streets)

Limited due to flood constraints; mostly small-scale renovations.

Strict building codes apply to new works or major renovations to ensure flood resilience, which can significantly increase construction costs.

Well-connected by road to the Bruce Highway and CBD. Local bus services are limited.

Walking distance to CBD shops, but the suburb itself lacks a major supermarket or retail hub.

Proximity to the Fitzroy River walks, though these are the first areas to close during rain events.

Depot Hill State School is a small, well-regarded local primary school. Older students usually travel to Rockhampton City or South Rockhampton.

Close to Rockhampton Hospital and various private clinics in the CBD (approx. 5-10 min drive).

A working-class demographic with a high percentage of single-person households and renters.

The high rental population and lower income levels suggest a market sensitive to cost-of-living pressures and rental price ceilings.

Development is largely restricted by the Rockhampton Regional Council's flood management strategies.

- Ongoing CBD riverfront revitalisation nearby increases local appeal.

- Rockhampton Ring Road project improving regional connectivity.

- Upgrades to local drainage and pump stations.

- Lack of new residential development due to insurance/finance hurdles.

- Potential for future 'buy-back' schemes in high-risk zones.

Residents are resilient and value the suburb's affordability and proximity to the city, but there is a constant underlying anxiety regarding the river levels.

We all look out for each other when the river rises. You won't find a cheaper place to live this close to town.

The yields are incredible, but you have to be prepared for the maintenance and the insurance headaches.

- Obtain an unconditional insurance quote before signing any contract.

- Check the Rockhampton Regional Council flood maps for the specific house level, not just the street.

- Prioritize 'high-set' homes where the living area is above the 1-in-100-year flood level.

- Inspect the condition of the stumps (concrete vs timber) thoroughly.

- Be prepared for a difficult resale process in the future.

- What was the exact water height inside or under this house during the 2017 flood?

- Can you provide a list of insurers currently providing flood cover for this specific address?

- Are the stumps original timber, or have they been replaced with concrete or steel?

- Is the lower level legal height, and has it ever been inundated?

- What is the current vacancy rate for your agency in this specific pocket?

- Are there any known structural issues caused by soil movement after floods?

- Provide a recent building and pest report to build buyer confidence.

- Highlight any flood-resilient renovations (e.g., steel stumps, water-resistant materials).

- Market the property specifically to cash-ready investors.

- Be realistic about the 'flood discount' required to move the property.

Position the property as a high-yield investment vehicle or a 'mortgage-free' lifestyle opportunity for budget buyers, emphasizing heritage charm and CBD proximity.

High-cash-flow play for experienced investors who can self-insure or manage high premiums.

Total loss of rent during flood events and potential for significant capital works.

- Target properties with long-term tenants.

- Ensure the electrical box is located above peak flood levels.

- Budget for higher-than-average annual maintenance.

- Focus on the 'dry' side of the suburb if possible.

- Ask the landlord about the property's flood history.

- Have an evacuation plan ready for the summer wet season.

- Ensure your contents insurance specifically covers flood.

Very cheap rent for a location so close to the CBD.

Risk of displacement during major rain events.

- Install flood-resilient flooring (e.g., polished concrete or tiles) downstairs.

- Maintain clear gutters and drainage pipes.

- Keep a good relationship with neighbors to monitor the property during weather events.

Ensure all smoke alarms and electrical safety switches are compliant and positioned above flood lines where possible.

- Buyers are almost exclusively local or interstate yield-chasers.

- Finance is the biggest deal-killer in this postcode.

- Flood maps are the first thing every serious buyer asks for.

Heritage charm meets CBD convenience at an unbeatable price point.

Cash investors and first-home buyers with high risk tolerance.

This report is based on historical data and projections as of March 2026. It does not constitute financial or legal advice. Property investment in flood-prone areas carries significant risk. Always seek independent professional advice and verify all flood data with the local council.